On July 21, 2010, the Obama administration saw the Dodd-Frank Wall Street Reform and Consumer Protection Act take effect, much to the dismay of Republicans in both the house and the senate. The bill passed without one Republican vote in the House, with many conservative critics claiming that the 2,300-page bill was a worthless and dangerous expansion of the government’s regulatory powers on Wall Street.

Almost five years later, it turns out that those conservative voices were right.

Now, I do applaud the president for his overall “moderate-ness” on economic issues. While the president has promoted strict EPA regulation upon pollution control to the appeal of Democrats, at the same time, he has intentions to cut the corporate tax rate from 35 percent to 28 percent. Remember the president extending the Bush tax cuts for two years in 2010? These more conservative economic outlooks from the Obama administration should be applauded.

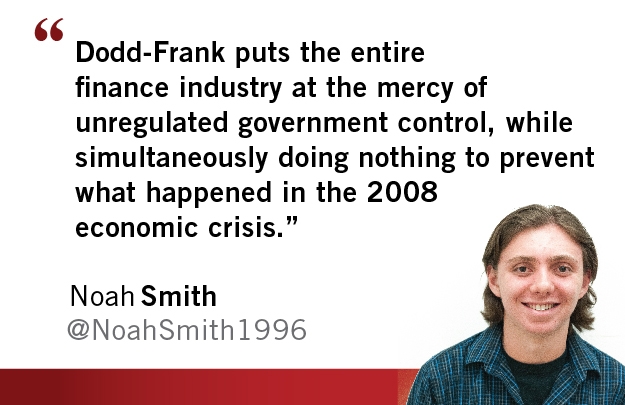

Dodd-Frank is an abomination on the financial sector: The bill puts American finance at the mercy of unregulated government control, while simultaneously doing absolutely nothing to prevent what caused the 2008 economic crisis.

The cause of much of the 2008 recession was that government housing policies made by Fannie Mae and Freddie Mac forced a reduction in mortgage underwriting standards. But Dodd-Frank does nothing about government housing polices to fix a broken housing-finance system. Instead the law goes out of its way to impose unnecessary regulations on financial firms. According to USA Today, Fannie Mae and Freddie Mac weren’t even mentioned in Dodd-Frank when it was originally conceived.

In fact, many provisions in Dodd-Frank deal with unrelated matters to the crisis. The “Durbin Amendment” in Title X sets price controls on fees banks can charge merchants in connection with debit cards. Another provision, Title IV, requires hedge-fund registration. Nowhere in Dodd-Frank is there any mention of provisions or rules that would fix housing finance; all these unnecessary rules only suffocate businesses in legal messes. In fact, according to US News, Dodd-Frank’s complex web of regulations favor large financial firms that can afford lawyers to analyze them, creating a set of rules that hurt businesses like smaller banks and credit rating agencies. Wow Dodd-Frank, thanks for being just about as worthless as the third "Godfather" movie.

When Dodd-Frank was first conceived, its main priority was to prevent American taxpayers from ever again having to bail out big banks because such failure from a major financial institution would have a severe impact on the economy. Essentially, we didn’t want our banks to get any bigger and avoid the possibility of a megabank tanking and taking the economy out with it. Both Republicans and Democrats saw the need to reinstate market discipline in the financial sector, a goal of Dodd-Frank legislation.

Forbes pointed at an analysis by Thomas Hoenig, vice chairman of the FDIC, which found that assets of the four largest U.S. banks amounted to 97 percent of the country’s gross domestic product in 2012. The findings show that since its inception in 2010, Dodd-Frank has done nothing to curb the “too big to fail problem.” What happens if any or all of banks suddenly experienced any sort of financial trouble? The largest problem with Dodd-Frank is that it has created the idea that these big financial firms are too large to fail, a dangerous gamble that has the making of another 2008 recession.

Reach the columnist at ndsmit12@asu.edu or follow @noahsmith1996 on Twitter.

Like The State Press on Facebook and follow @statepress on Twitter.

Editor’s note: The opinions presented in this column are the author’s and do not imply any endorsement from The State Press or its editors.

Want to join the conversation? Send an email to opiniondesk.statepress@gmail.com. Keep letters under 300 words and be sure to include your university affiliation. Anonymity will not be granted.